In order to have a view on whether the market is attractive or not, it's essential to consider the assumptions that are reflected in market pricing. What follows is a review of a variety of key market-based indicators that provide insights into the assumptions the market is making about the future. Taken together, these indicators suggest that the market is still quite cautious and concerned about the future. Nowhere is there any indication that the market is priced to optimistic or rosy assumptions about economic growth, inflation, interest rates or corporate profits. Indeed, most indicators reflect a market that is already discounting a deterioration in corporate profits, sharply rising yields, and/or higher corporate tax rates. What this suggests is that if the future turns out to be less problematic than the market is expecting, then there is still a lot of upside potential in equity prices.

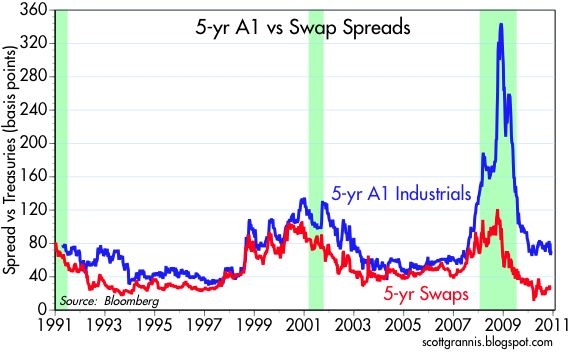

This chart compares the spread on 5-yr swaps (a measure of the credit risk of generic AA-rated banks) to the spread on 5-yr A1 Industrial corporations (a measure of the credit risk of generic industrial corporations). Swap spreads have been trading at "normal" levels for most of this year, but industrials are still trading at levels that are elevated in an historical context. This means that the market still worries (not a lot, but more than it would if the outlook were healthy) about the viability of large industrial corporations over the next several years.

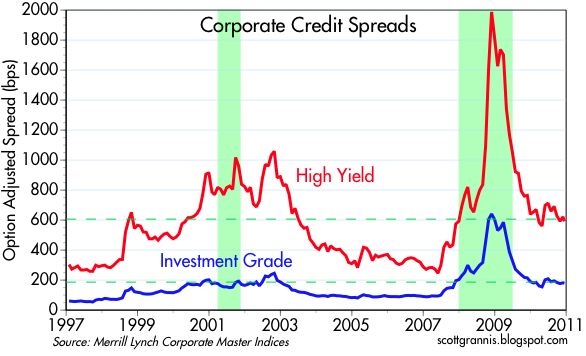

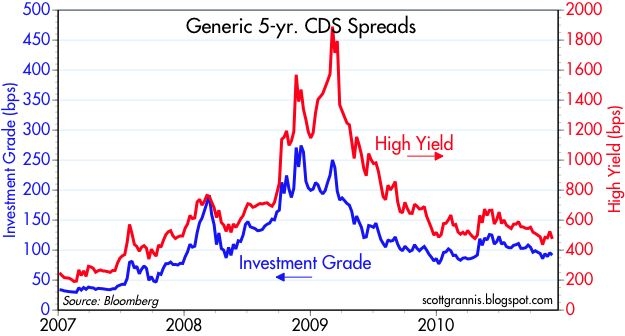

Credit default swaps tell a similar story to that of credit spreads in general: the market's perception of default risk is still substantially higher than it was prior to the onset of the 2008 recession.

Complete Story »

Tricia Helfer Elena Lyons Brooke Burns Lena Headey Ali Larter

No comments:

Post a Comment